- Lightspeed

- Posts

- 🪐 Jupiter is saving its token

Brought to you by:

hello

We’re looking at Jupiter today, the center of the Solana DeFi ecosystem. Revenues are going up, but JUP’s token price goes the other way. Does anyone have an answer?

Inside the Jupiterverse

Less than two years ago, Jupiter was “just” a DEX aggregator. Today, the company looks more like a DeFi conglomerate, or a “Superapp.”

On top of its flagship spot aggregator, the team runs perps, a memecoin launchpad, the JLP liquidity pool, lending, liquid staking, a portfolio tracker, a RFQ venue (JupiterZ), developer APIs, a token verification system (Verify) and the third-largest Solana validator.

Source: Jupiter

Too many? That’s not yet including the pipeline of emerging products: a jupUSD stablecoin, a prediction market in partnership with Kalshi, an ICO launchpad (Jupiter DTF) and its “omnichain” network JupNet. I’m probably still missing some.

Jupiter’s suite of products is not inactive shelfware, either. Almost every product stands on its own. In its Q3 token holder update yesterday, the team pegs Q3 revenue at ~$45 million — ~$180 million annualized.

For a crypto business, that’s real money.

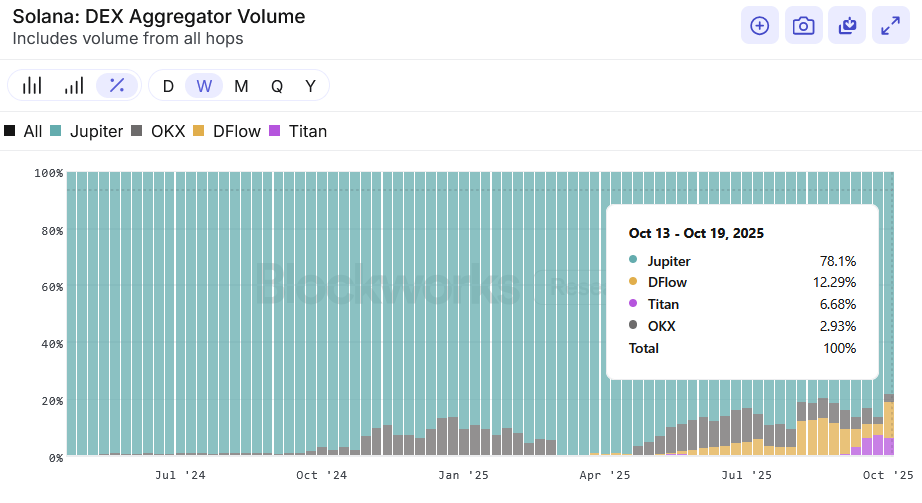

Jupiter’s DEX aggregator dominates Solana DeFi

But while Jupiter is firing on all cylinders, there’s an uncomfortable truth: The JUP token hasn’t kept up. JUP sits at around a $1.1 billion market cap today, down from $3 billion at its peak earlier this year, or a ~6.2x P/S.

In my conversations with Solana traders and investors, everyone has a different explanation for why the token of Solana’s most prominent protocol hasn’t performed well this year.

Some cited the token’s lack of utility. One liquid fund told me that JUP was perceived as too “safe” for speculative money; others pointed to the fact that JUP’s buybacks were too small relative to its FDV.

The pseudonymous founder of Elemental, Moo, gave me a simpler take: “Jupiter had an ‘Avengers’ moment where all the hype the team built culminated in last year’s Catstanbul event.”

“Given the level of hype, a correction was inevitable. And when prices drop, people start questioning everything. The community’s main concern now seems to be whether Jupiter's growth plans will be enough to reignite interest in the token. Jupiter has a grand vision, but it will take time to execute.”

Jupiter also has something of a complexity tax, a similar problem that Ethereum suffers from.

When a company spans a dozen interrelated businesses, the story gets harder to model, and markets often apply a discount until the value capture is obvious.

I’d love to see an investment analyst brave enough to publish a sum-of-parts model for Jupiter’s product zoo.

To the team’s credit, they seem to recognize these problems and are taking steps to rectify it.

In the team’s Q3 token holders update last night, the Jupiter team called for a “fresh start for JUP” and outlined moves aimed at tighter focus: scaling back DAO voting to only "major tokenomics and treasury decisions", cutting the JUP unstaking period from 30 days to seven, and — pending governance — burning 121 million JUP (~$42 million) from the Litterbox strategic reserve.

“Some of the mechanics around [the] JUP token were preventing people from getting engaged. We want to fix that. Some of the overemphasis and overfocus on the comms side around the DAO was turning people off and creating a negative attention flywheel. Don't want to do that anymore,” Dhanda said on the livestream.

Jupiter has built a rare thing in crypto, an operating business that throws off cash across multiple product lines.

Markets are for now pricing the token like a safe, sprawling operator rather than a single, spicy bet. If Jupiter can make the value path to JUP simpler, maybe it can change the fate of its token too.

Brought to you by:

Katana was built by answering a core question: What if a chain contributed revenue back into the ecosystem to drive growth and yield?

We direct revenue back to DeFi participants for consistently higher yields.

Katana is pioneering concepts like Productive TVL (the portion of assets are actually doing work), Chain Owned Liquidity (permanent liquidity owned by Katana to maintain stability), and VaultBridge (putting bridged assets to work generating extra yield for active participants).

Prop AMM dominance:

The above chart illustrates the dominance of prop AMMs over Solana. For weeks, prop AMMs have consistently processed more trading volumes than public AMMs via DEX aggregators. In the last week alone, prop AMMs processed 3x more volumes than public AMMs — $14.9 billion over $4.4 billion.