- Lightspeed

- Posts

- 😅 No sweat

Howdy!

Just a few more days until Jack is back from his jaunt in the English countryside. Until then, enjoy a breakdown of Polymarket’s Election Day performance and an update on SOL issuance:

Polymarket didn’t break

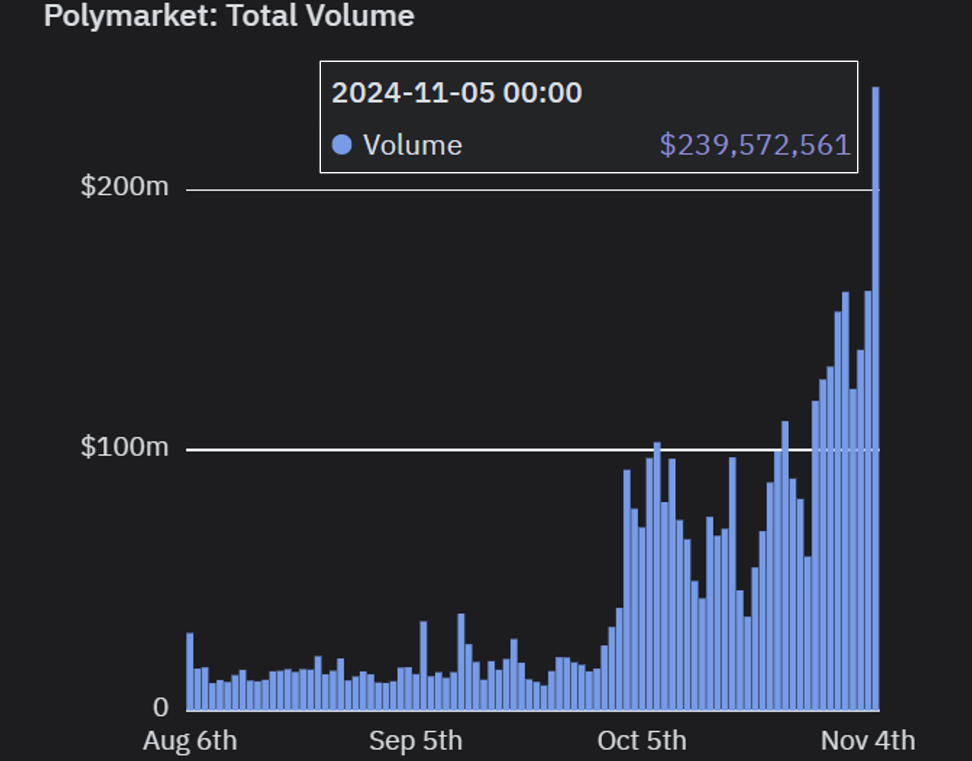

On the most important night of the year for Polymarket, crypto’s breakout star application processed $240 million in trading volumes without any problems.

Source: Blockworks Research

It’s an impressive feat for a dapp that is mostly onchain, representing perhaps one of crypto’s first “mainstream” tests.

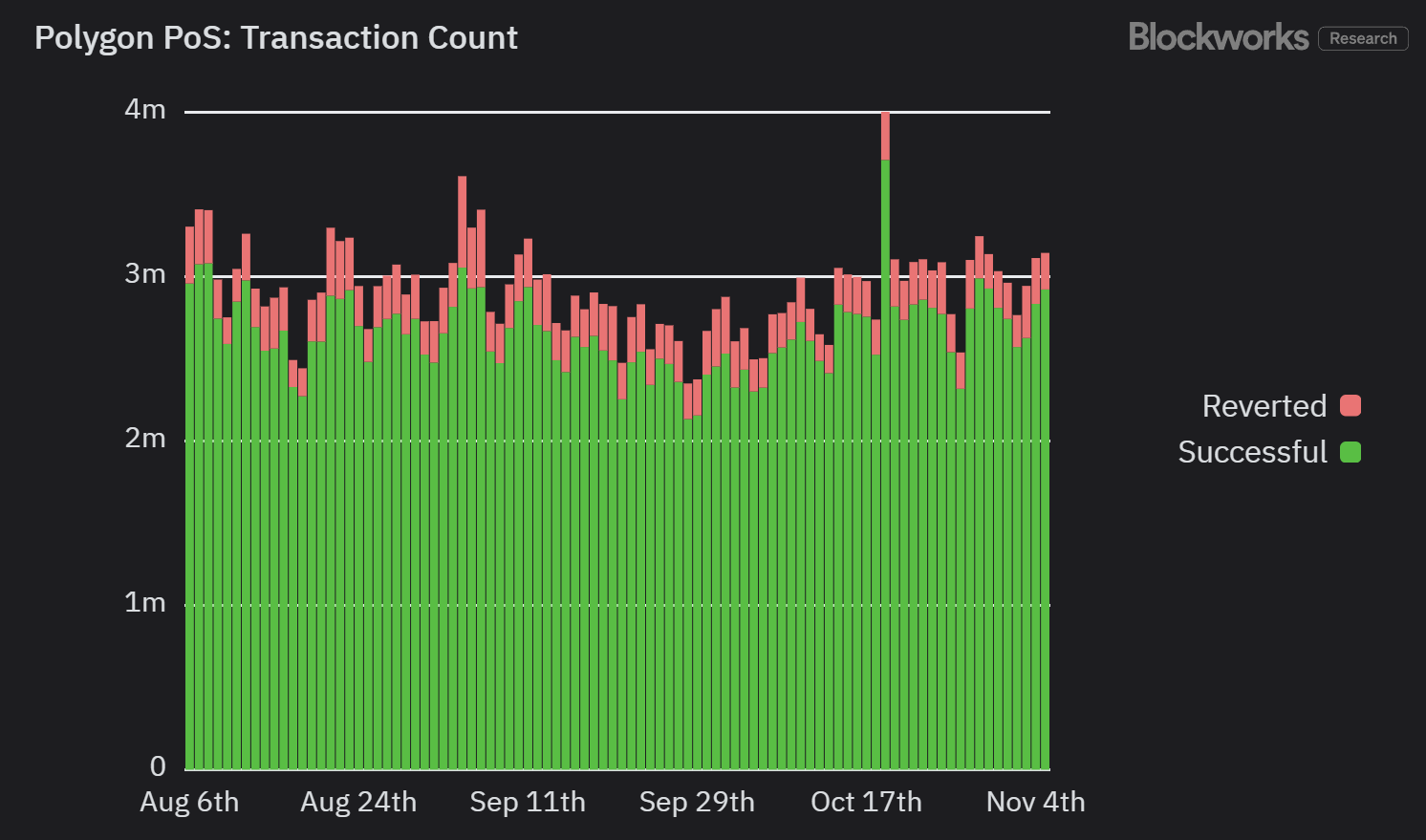

Polymarket is designed as a "binary limit order book” (BLOB), a kind of hybrid-decentralized model that is common in many DEXs. Matching (i.e. placing limit orders) on Polymarket is offchain, while settlement and execution of trades goes onchain on Polygon’s PoS sidechain.

The underlying blockchain chugged along more or less smoothly, processing 2,921,668 transactions on election day, or about 33.8 TPS at a 7% reversion rate, Blockworks Research data shows.

Source: Blockworks Research

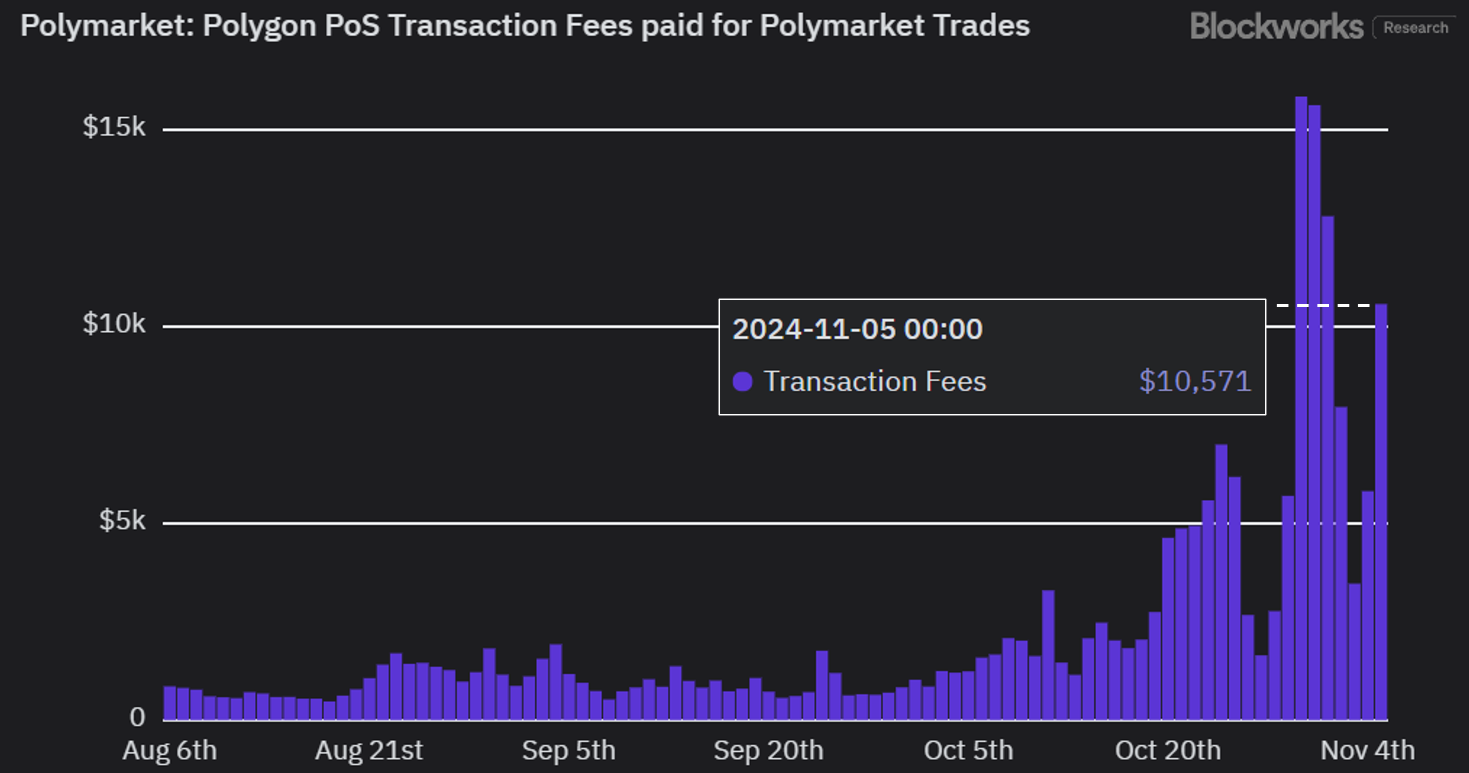

Polygon is taking many well-deserved victory laps, but what’s not talked about is how little value has accrued to its POL token despite Polymarket’s success. On election day alone, Polymarket users generated a pretty minor $10,571 in fees for Polygon.

The price of POL (previously MATIC) is up 7.2% on the day at $0.3, but still down about 54% year to date.

Source: Blockworks Research

This is not a knock on Polygon; Polygon’s sidechain design was aimed at delivering ultra-low fees at a time when L2s were still relatively scarce.

Polygon’s bet on POL’s value accrual is aimed at the token’s utility in staking for various different Polygon-related services like block batching in the Agglayer, or providing data availability within its Staking Hub/Layer in 2025.

The plan is also to let POL stakers derive fee revenue from other Polygon CDK chains within its aggregated network of blockchains.

But back to Polymarket — where does the prediction market go from here?

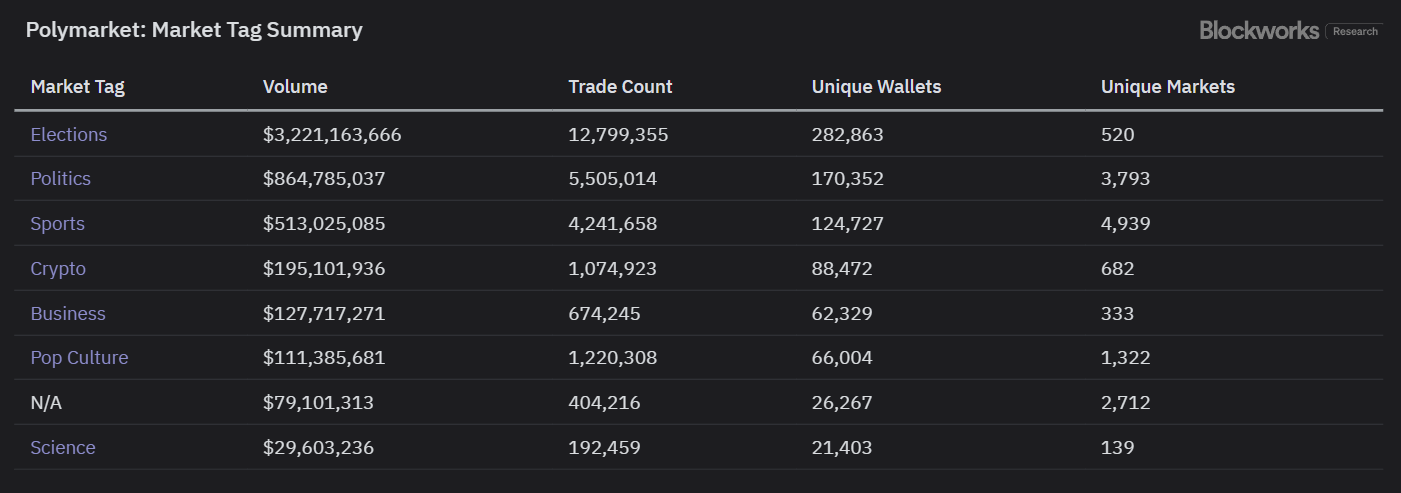

The majority of Polymarket’s usage comes from US political elections. Post-election, Polymarket’s continued success will have to rely on other areas of interest that can stoke the same kind of mainstream appetite as political gambling.

Source: Blockworks Research

Sports, which makes up the third-largest category of open interest on Polymarket, is one possible demand driver, but that area of gambling is also saturated with existing crypto players like Shuffle, Gandom, Rollbit, Stake.com and more, as well as a slew of Web2 offerings.

For more on Polymarket’s next steps, plug into the latest 0xResearch podcast episode.

— Donovan Choy

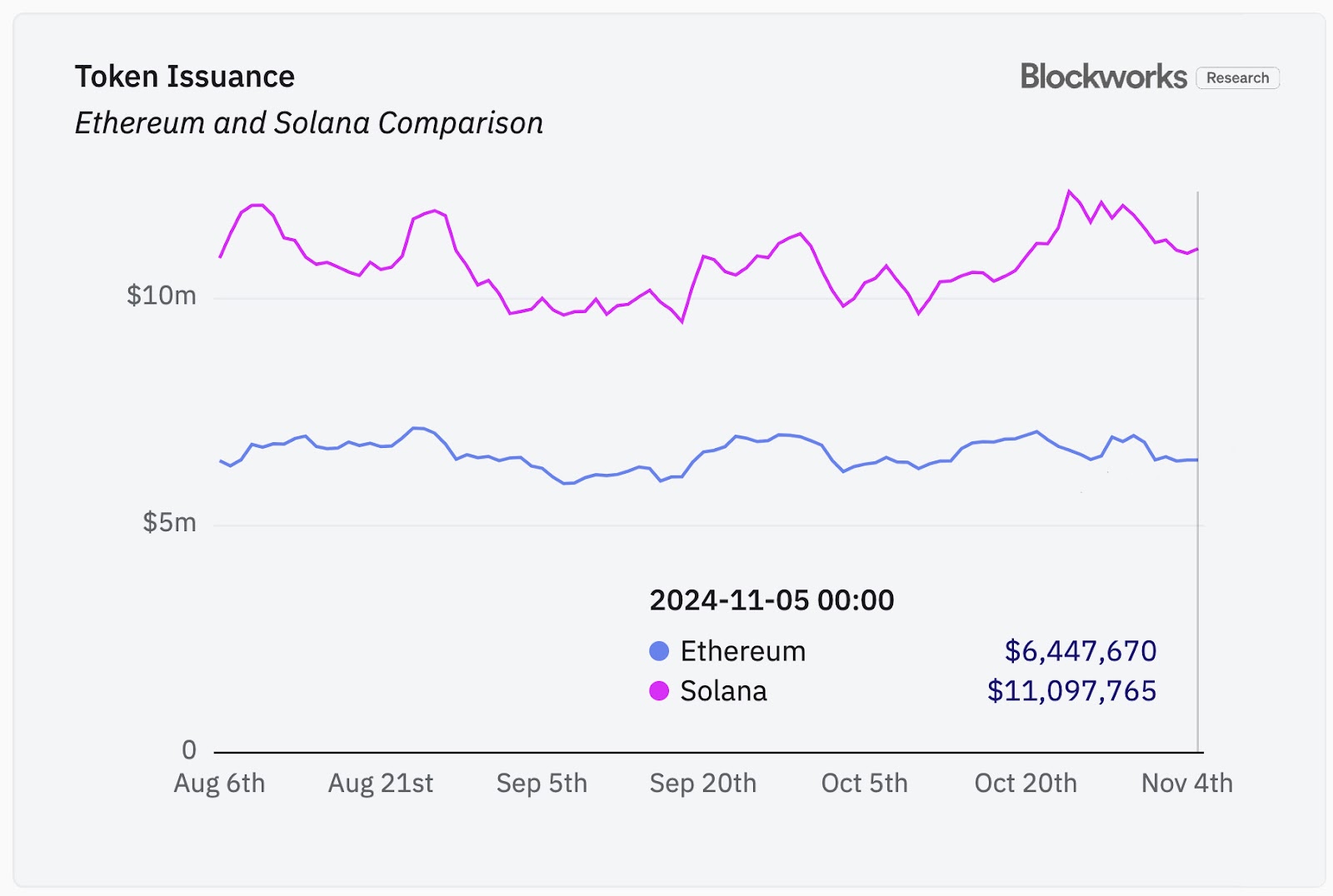

Solana vs Ethereum issuance:

Source: Blockworks Research

Ethereum (ETH) and Solana (SOL) have distinct issuance models impacting their supply dynamics. Ethereum follows a decreasing issuance model, post-Merge, with rewards solely from staking. This model, combined with ETH’s burn mechanism from EIP-1559, has led to net deflation in its supply — currently about -0.04% per year.

Solana, however, operates with a fixed issuance rate, rewarding validators and increasing SOL supply at a predictable rate — an annual inflation rate of currently 5.145%, which decreases by 15% each year until reaching a long-term rate of 1.5%.

This consistent inflation supports network security and incentivizes participation but contrasts Ethereum’s deflationary leanings.

— Macauley Peterson

Are you happy with the results of the US election? |